U.S. Dairy Exports Update – Oct ’19

Executive Summary

U.S. dairy export figures provided by USDA were recently updated with values spanning through Aug ’19. Highlights from the updated report include:

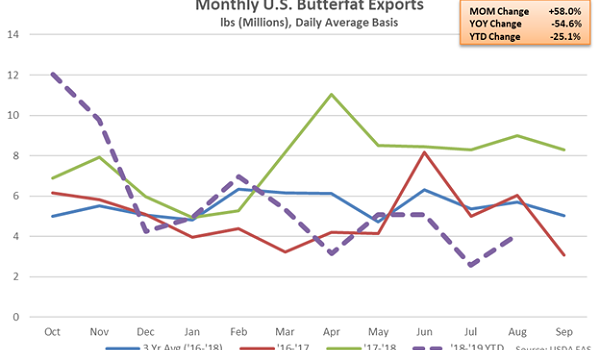

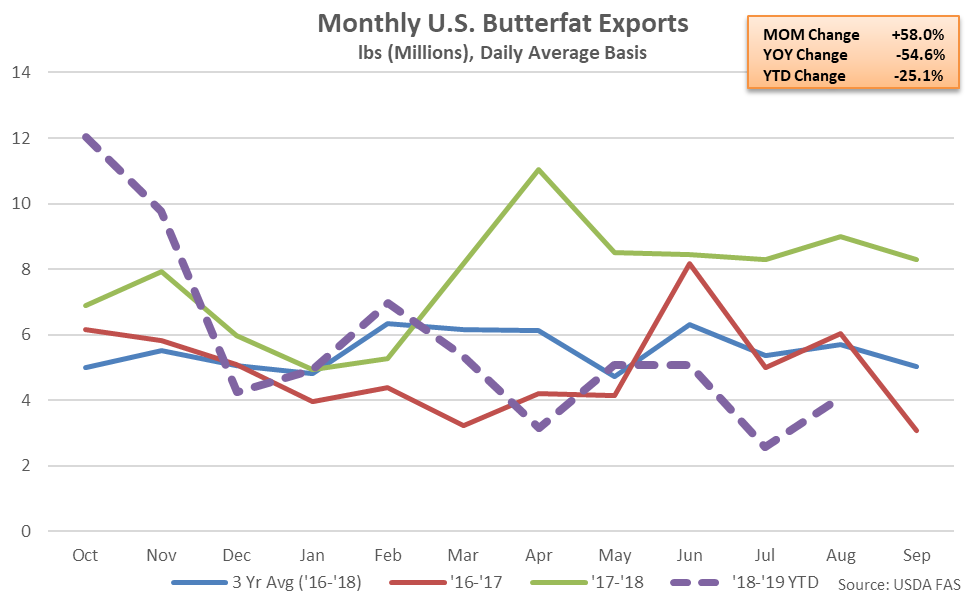

Butterfat export volumes destined to Mexico, Canada and the EU-28 declined most significantly on a YOY basis throughout the month, while export volumes destined to South Korea finished most significantly higher.

Butterfat export volumes destined to Mexico, Canada and the EU-28 declined most significantly on a YOY basis throughout the month, while export volumes destined to South Korea finished most significantly higher.

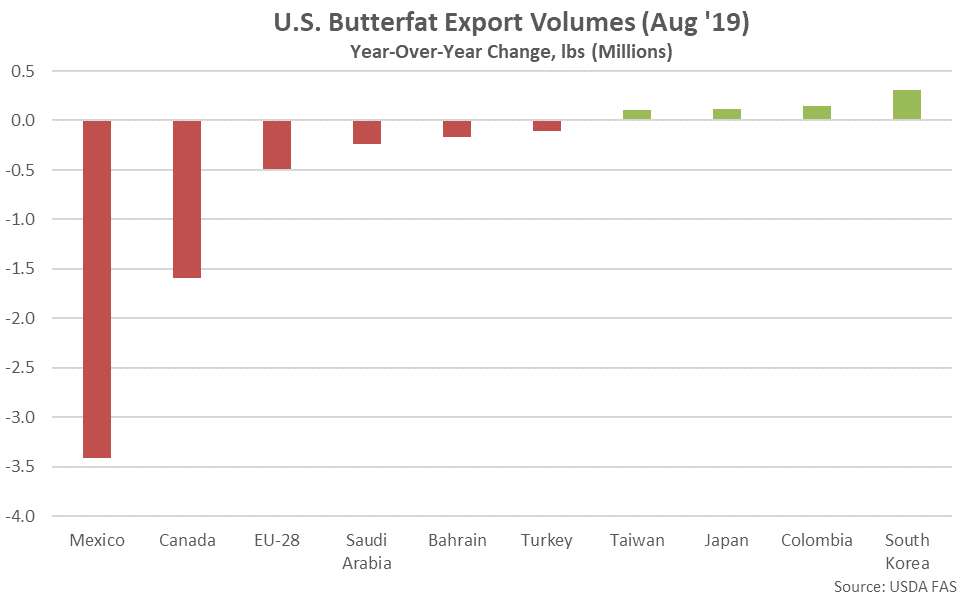

Canada and Mexico have historically been the largest importers of U.S. cheese, accounting for 55% of total U.S. butterfat export volumes throughout the past five years. U.S. butterfat export volumes destined to Canada and Mexico have declined by 27.0% and 1.6%, respectively, on a YOY basis throughout the past 12 months, compared to a 22.7% YOY decline in U.S. butterfat export volumes destined to all other countries.

Canada and Mexico have historically been the largest importers of U.S. cheese, accounting for 55% of total U.S. butterfat export volumes throughout the past five years. U.S. butterfat export volumes destined to Canada and Mexico have declined by 27.0% and 1.6%, respectively, on a YOY basis throughout the past 12 months, compared to a 22.7% YOY decline in U.S. butterfat export volumes destined to all other countries.

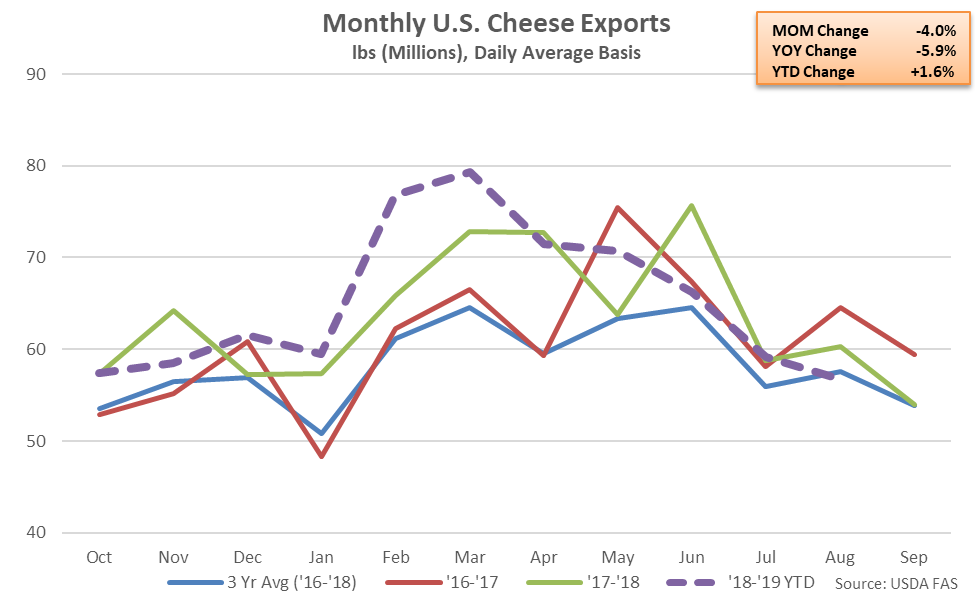

Cheese – Export Volumes Decline 5.9% YOY to a Three Year Seasonal Low Level

Aug ’19 U.S. cheese export volumes declined on a YOY basis for the second time in the past three months, finishing down 5.9% to a three year seasonal low level. Cheddar cheese export volumes declined 44.1% YOY throughout the month, more than offsetting a 2.6% YOY increase in other-than-cheddar cheese export volumes experienced throughout the month. ’17-’18 annual cheese export volumes finished up 4.1% YOY to a four year high, despite declining by 4.9% on a YOY basis over the final quarter of the production season. ’18-’19 YTD cheese export volumes remain up an additional 1.6% YOY heading into the final month of the production season, despite the most recent YOY decline.

Cheese – Export Volumes Decline 5.9% YOY to a Three Year Seasonal Low Level

Aug ’19 U.S. cheese export volumes declined on a YOY basis for the second time in the past three months, finishing down 5.9% to a three year seasonal low level. Cheddar cheese export volumes declined 44.1% YOY throughout the month, more than offsetting a 2.6% YOY increase in other-than-cheddar cheese export volumes experienced throughout the month. ’17-’18 annual cheese export volumes finished up 4.1% YOY to a four year high, despite declining by 4.9% on a YOY basis over the final quarter of the production season. ’18-’19 YTD cheese export volumes remain up an additional 1.6% YOY heading into the final month of the production season, despite the most recent YOY decline.

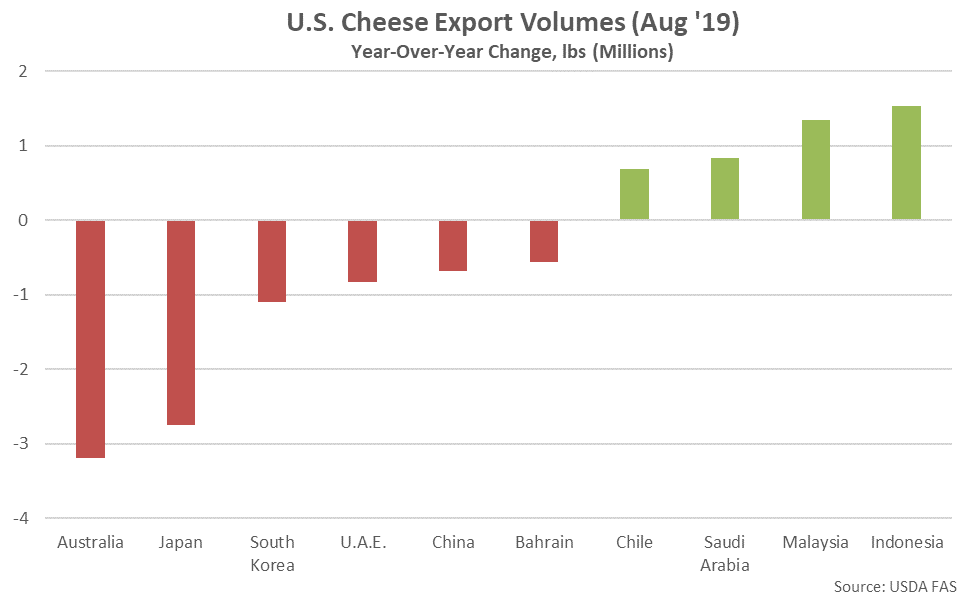

Aug ’19 YOY declines in cheese export volumes were led by product destined to Australia and Japan, while volumes destined to Indonesia finished most significantly higher on a YOY basis throughout the month.

Aug ’19 YOY declines in cheese export volumes were led by product destined to Australia and Japan, while volumes destined to Indonesia finished most significantly higher on a YOY basis throughout the month.

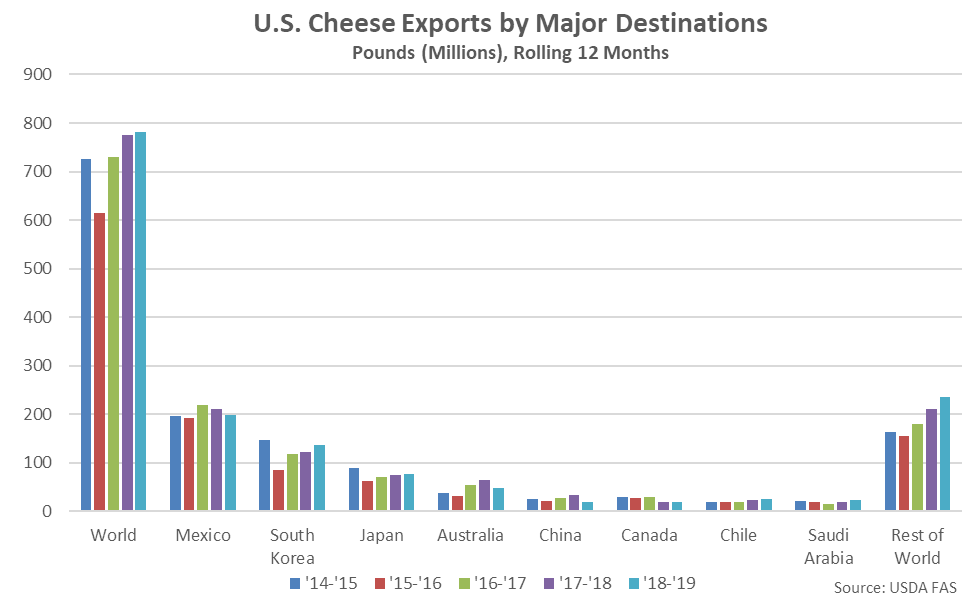

Mexico and South Korea have historically been the largest importers of U.S. cheese, accounting for 45% of total U.S. cheese export volumes throughout the past five years. Combined U.S. cheese export volumes destined to Mexico and South Korea have increased 0.4% on a YOY basis throughout the past 12 months.

Mexico and South Korea have historically been the largest importers of U.S. cheese, accounting for 45% of total U.S. cheese export volumes throughout the past five years. Combined U.S. cheese export volumes destined to Mexico and South Korea have increased 0.4% on a YOY basis throughout the past 12 months.

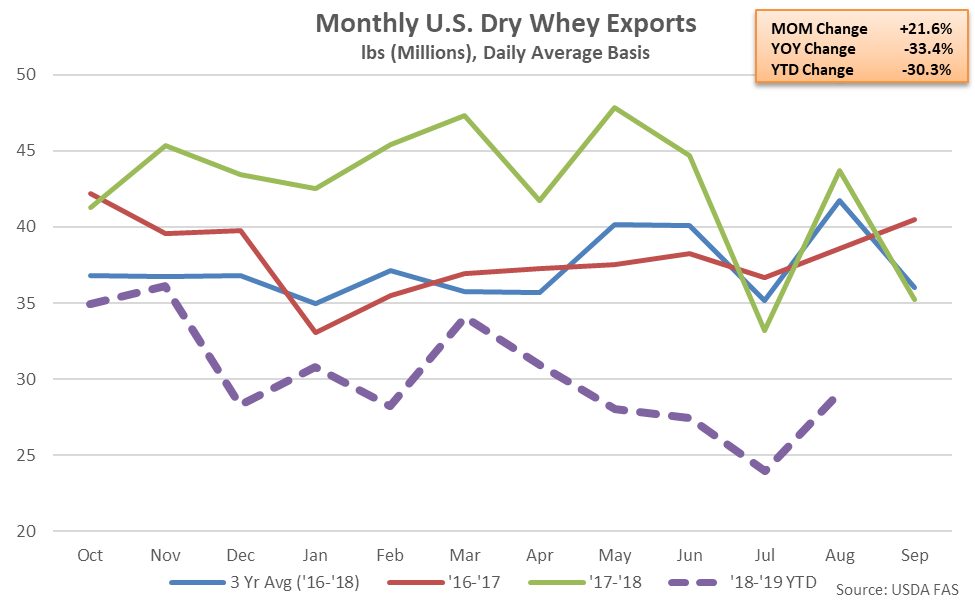

Whey – Total Export Volumes Remain Lower YOY on Weak Chinese Demand

Aug ’19 U.S. dry whey export volumes remained lower on a YOY basis for the 12th consecutive month, declining by 33.4% to a 16 year seasonal low level. ’17-’18 annual dry whey export volumes finished up 12.3% YOY to a four year high, despite declining by 3.0% on a YOY basis over the final quarter of the production season. ’18-’19 YTD dry whey export volumes have declined 30.3% YOY heading into the final month of the production season, however.

Whey – Total Export Volumes Remain Lower YOY on Weak Chinese Demand

Aug ’19 U.S. dry whey export volumes remained lower on a YOY basis for the 12th consecutive month, declining by 33.4% to a 16 year seasonal low level. ’17-’18 annual dry whey export volumes finished up 12.3% YOY to a four year high, despite declining by 3.0% on a YOY basis over the final quarter of the production season. ’18-’19 YTD dry whey export volumes have declined 30.3% YOY heading into the final month of the production season, however.

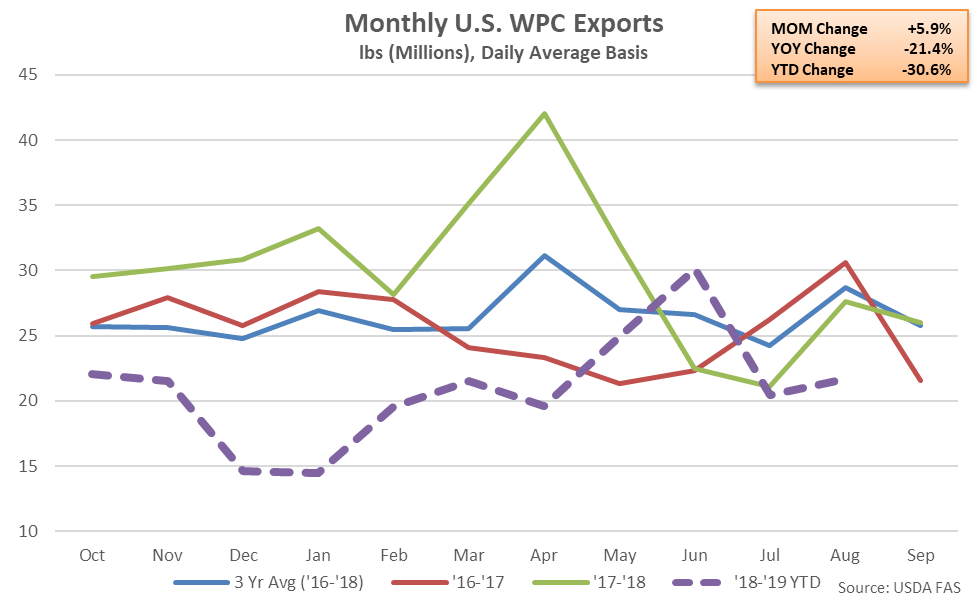

Aug ’19 whey protein concentrate (WPC) export volumes finished lower on a YOY basis for the tenth time in the past 11 months, declining by 21.4% to a four year seasonal low level. ’17-’18 annual WPC export volumes finished up 17.4% YOY, reaching a record annual high level for the third consecutive year, despite declining by 4.7% on a YOY basis over the final quarter of the production season. ’18-’19 YTD WPC export volumes have declined 30.6% YOY heading into the final month of the production season, however, and are on pace to reach a four year low level.

Aug ’19 whey protein concentrate (WPC) export volumes finished lower on a YOY basis for the tenth time in the past 11 months, declining by 21.4% to a four year seasonal low level. ’17-’18 annual WPC export volumes finished up 17.4% YOY, reaching a record annual high level for the third consecutive year, despite declining by 4.7% on a YOY basis over the final quarter of the production season. ’18-’19 YTD WPC export volumes have declined 30.6% YOY heading into the final month of the production season, however, and are on pace to reach a four year low level.

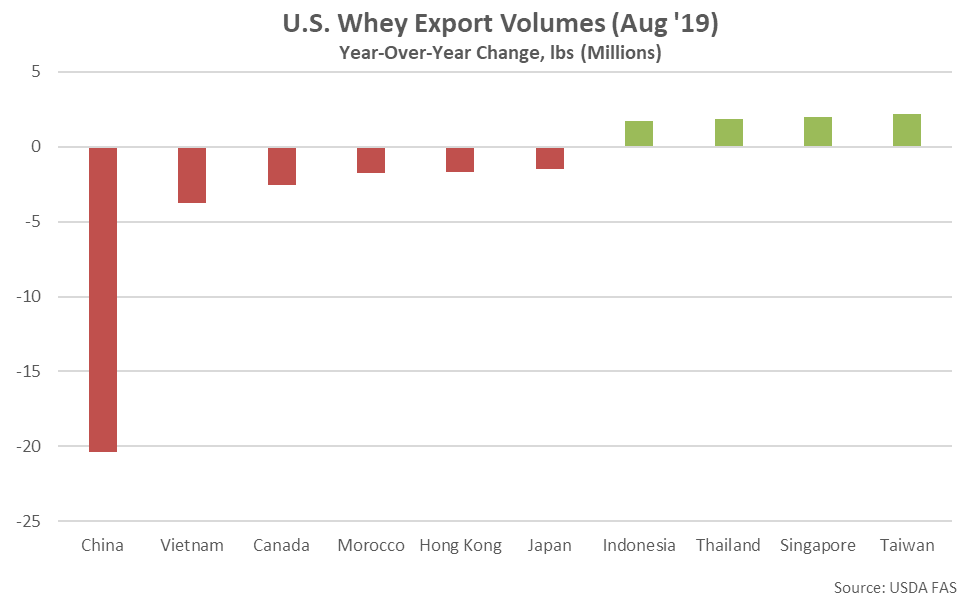

U.S. whey export volumes destined to China declined most significantly on a YOY basis throughout the month, finishing down 65.6%. Excluding China, Aug ’19 U.S. whey export volumes declined by just 5.7% on a YOY basis. China applied a 25% retaliatory tariff to a wide variety of U.S. dairy products including whey during early Jul ’18 while Chinese whey demand has also been reduced on weaker feed demand due to African swine fever.

U.S. whey export volumes destined to China declined most significantly on a YOY basis throughout the month, finishing down 65.6%. Excluding China, Aug ’19 U.S. whey export volumes declined by just 5.7% on a YOY basis. China applied a 25% retaliatory tariff to a wide variety of U.S. dairy products including whey during early Jul ’18 while Chinese whey demand has also been reduced on weaker feed demand due to African swine fever.

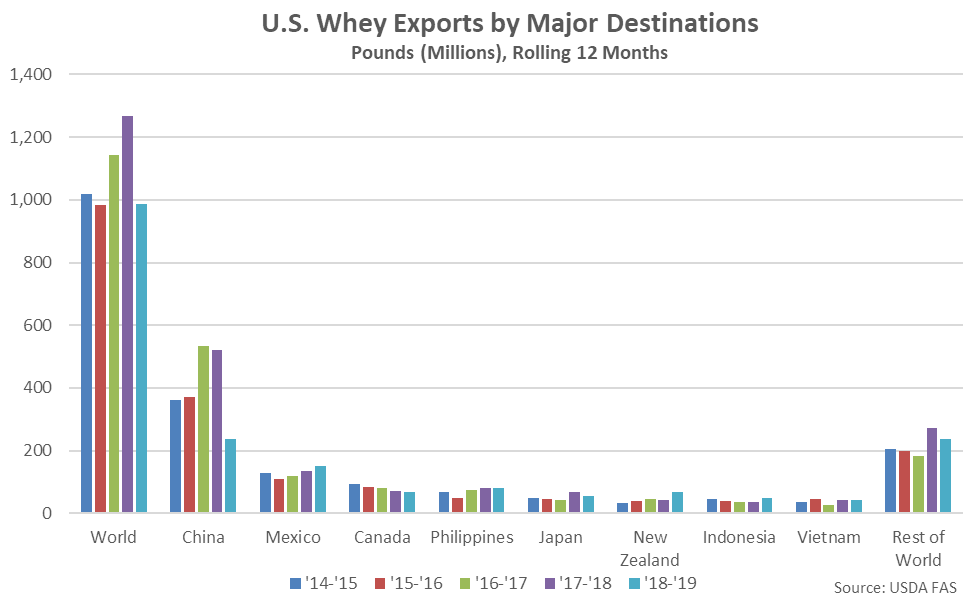

China has historically been the largest importer of U.S. whey products, accounting for nearly 40% of total U.S. whey export volumes throughout the past five years. U.S. whey export volumes destined to China have declined 54.3% YOY throughout the past 12 months, more than offsetting a 0.5% YOY increase in whey export volumes destined to all other countries.

China has historically been the largest importer of U.S. whey products, accounting for nearly 40% of total U.S. whey export volumes throughout the past five years. U.S. whey export volumes destined to China have declined 54.3% YOY throughout the past 12 months, more than offsetting a 0.5% YOY increase in whey export volumes destined to all other countries.

NFDM/SMP – Export Volumes Decline YOY for the Tenth Consecutive Month, Finish Down 18.3%

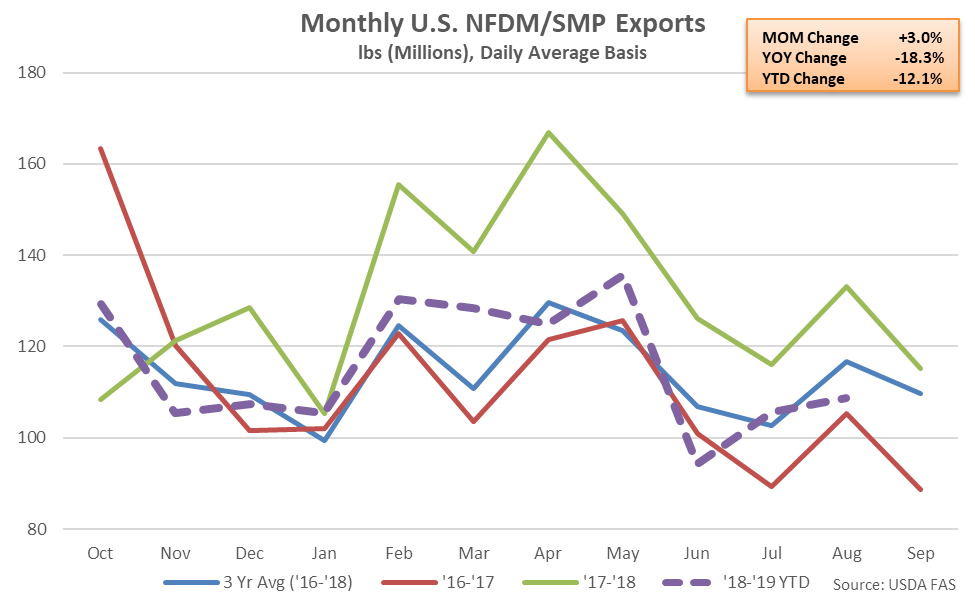

Aug ’19 U.S. export volumes of nonfat dry milk (NFDM) and skim milk powder (SMP) remained lower on a YOY basis for the tenth consecutive month, finishing down 18.3%. ’17-’18 annual NFDM/SMP exports finished up 16.4% YOY, reaching a record annual high level for the second consecutive year, however ’18-’19 YTD NFDM/SMP export volumes have declined by 12.1% YOY heading into the final month of the production season.

NFDM/SMP – Export Volumes Decline YOY for the Tenth Consecutive Month, Finish Down 18.3%

Aug ’19 U.S. export volumes of nonfat dry milk (NFDM) and skim milk powder (SMP) remained lower on a YOY basis for the tenth consecutive month, finishing down 18.3%. ’17-’18 annual NFDM/SMP exports finished up 16.4% YOY, reaching a record annual high level for the second consecutive year, however ’18-’19 YTD NFDM/SMP export volumes have declined by 12.1% YOY heading into the final month of the production season.

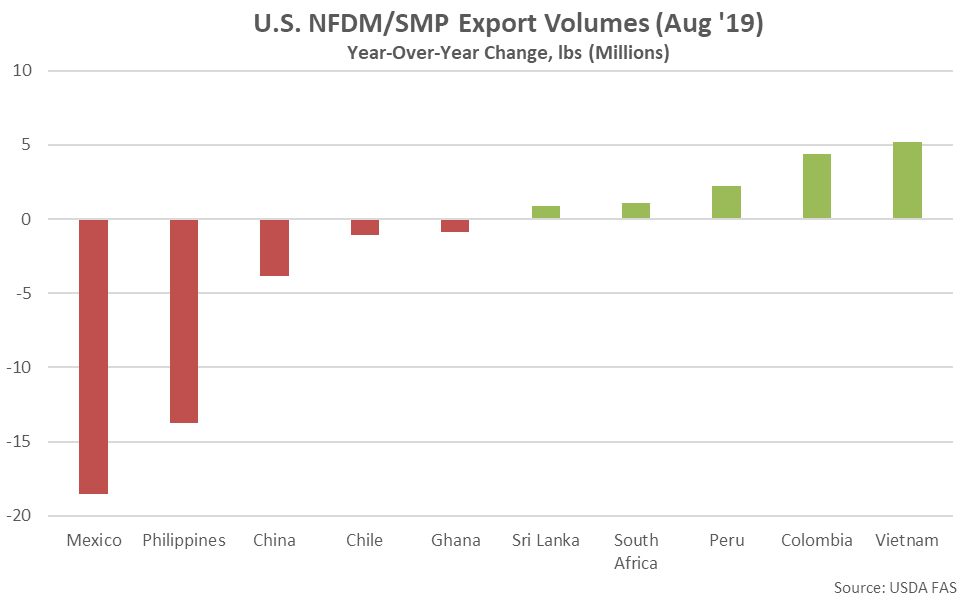

Aug ’19 YOY declines in NFDM/SMP export volumes were led by product destined to Mexico and the Philippines, while export volumes destined to Vietnam and Columbia finished most significantly higher on a YOY basis throughout the month.

Aug ’19 YOY declines in NFDM/SMP export volumes were led by product destined to Mexico and the Philippines, while export volumes destined to Vietnam and Columbia finished most significantly higher on a YOY basis throughout the month.

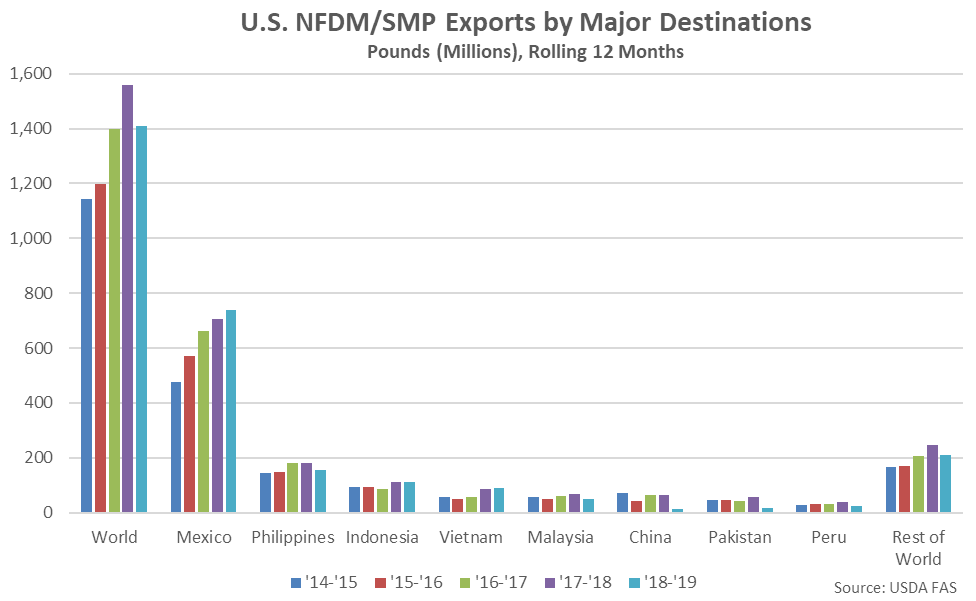

Mexico has historically been the largest importer of U.S. NFDM/SMP, accounting for nearly half of all U.S. NFDM/SMP export volumes throughout the past five years. U.S. NFDM/SMP export volumes destined to Mexico have increased 4.5% YOY throughout the past 12 months however export volumes destined to all other countries have declined by 21.3% on a YOY basis over the same period.

Mexico has historically been the largest importer of U.S. NFDM/SMP, accounting for nearly half of all U.S. NFDM/SMP export volumes throughout the past five years. U.S. NFDM/SMP export volumes destined to Mexico have increased 4.5% YOY throughout the past 12 months however export volumes destined to all other countries have declined by 21.3% on a YOY basis over the same period.

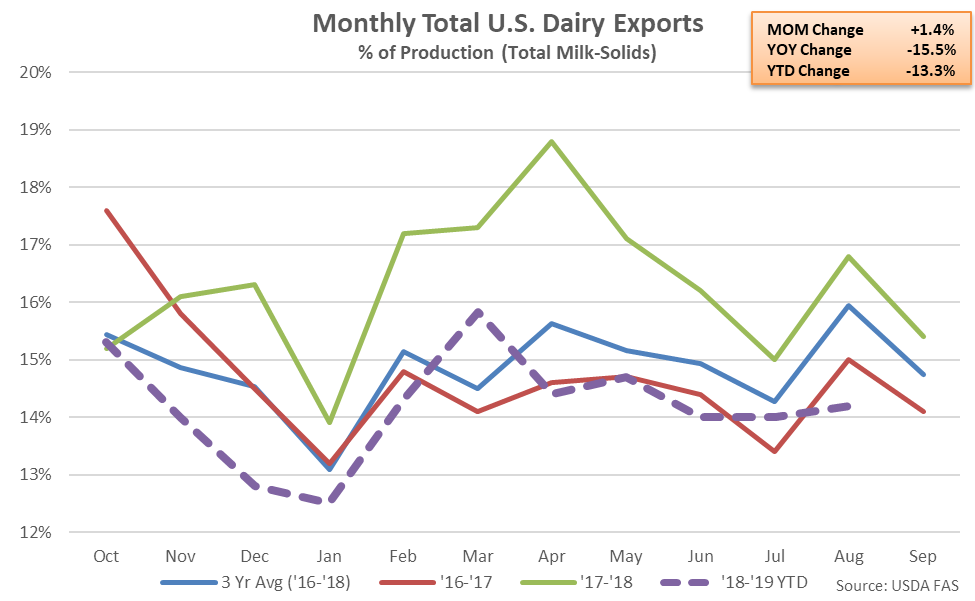

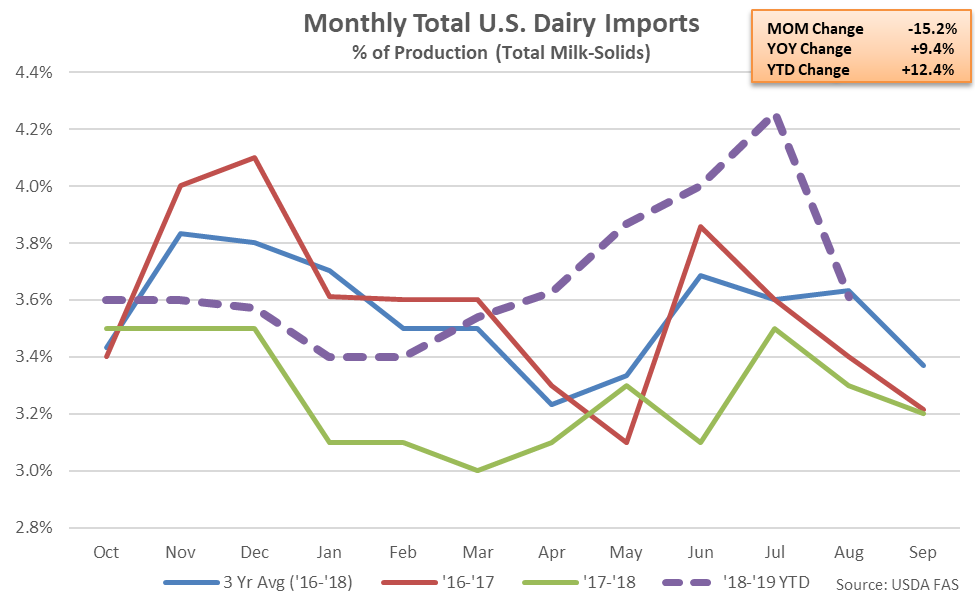

Export Volumes Normalized to Production

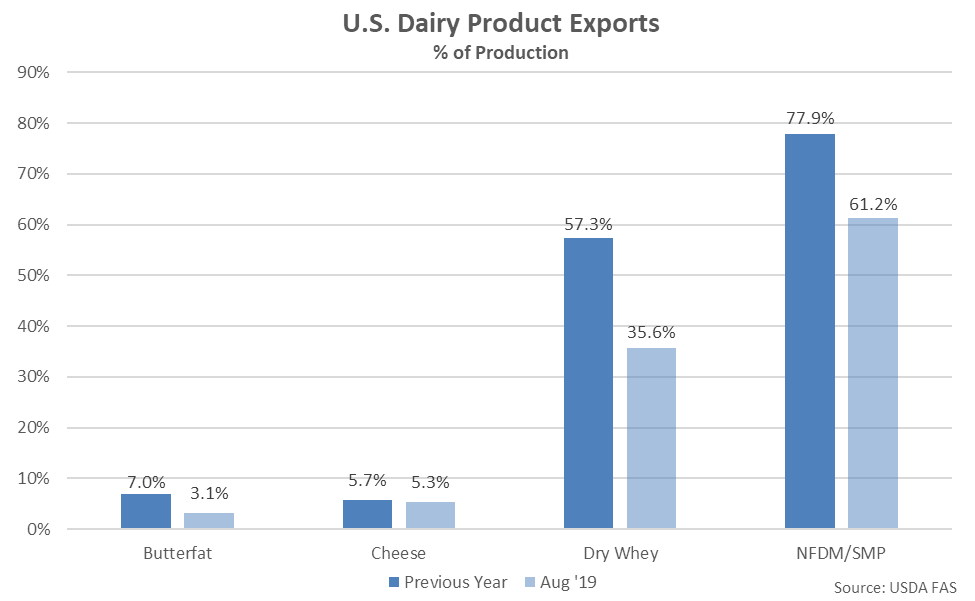

U.S. butterfat, cheese, dry whey and NFDM/SMP export volumes as a percentage of production all finished below previous year figures during Aug ’19. Dry whey export volumes as a percentage of production finished most significantly lower on a YOY basis throughout the month.

Export Volumes Normalized to Production

U.S. butterfat, cheese, dry whey and NFDM/SMP export volumes as a percentage of production all finished below previous year figures during Aug ’19. Dry whey export volumes as a percentage of production finished most significantly lower on a YOY basis throughout the month.

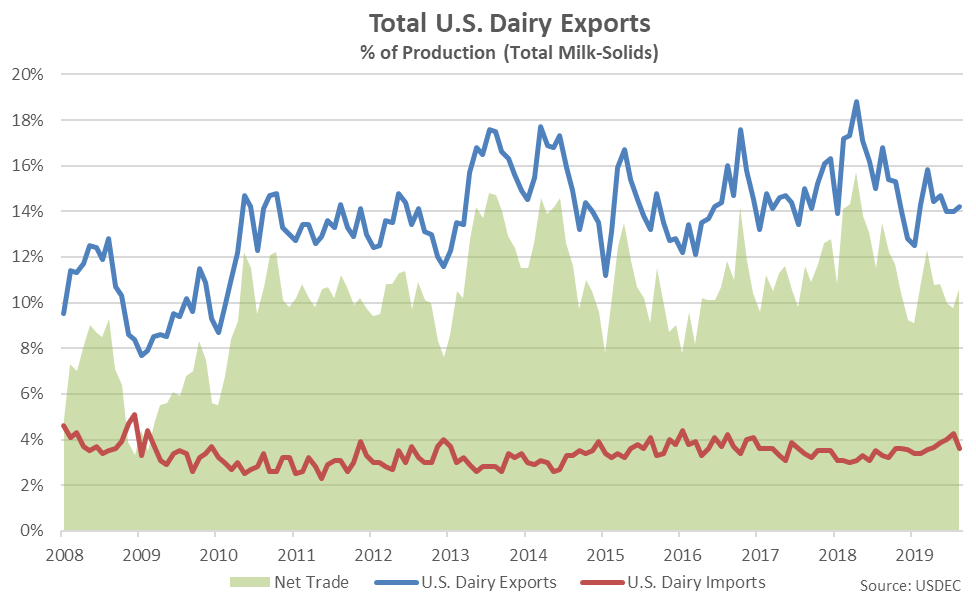

Overall, U.S. dairy export volumes were estimated to be equivalent to approximately 14.2% of total U.S. milk-solids production during Aug ’19 while dairy import volumes were estimated to be equivalent to approximately 3.6% of total U.S. milk-solids production. Aug ’19 net dairy trade finished 21.5% lower YOY, declining for the tenth consecutive month.

Overall, U.S. dairy export volumes were estimated to be equivalent to approximately 14.2% of total U.S. milk-solids production during Aug ’19 while dairy import volumes were estimated to be equivalent to approximately 3.6% of total U.S. milk-solids production. Aug ’19 net dairy trade finished 21.5% lower YOY, declining for the tenth consecutive month.

Aug ’19 U.S. dairy exports as a percentage of milk-solids production remained lower on a YOY basis for the tenth consecutive month, finishing down 15.5%. ’17-’18 annual dairy exports as a percentage of milk-solids production finished at a record high value of 16.3%, however ’18-’19 YTD figures have declined 13.3% YOY heading into the final month of the production season.

Aug ’19 U.S. dairy exports as a percentage of milk-solids production remained lower on a YOY basis for the tenth consecutive month, finishing down 15.5%. ’17-’18 annual dairy exports as a percentage of milk-solids production finished at a record high value of 16.3%, however ’18-’19 YTD figures have declined 13.3% YOY heading into the final month of the production season.

Aug ’19 U.S. dairy imports as a percentage of milk-solids production declined from the three and a half year high experienced throughout the previous month but remained higher on a YOY basis for the 11th consecutive month, finishing up 9.4%. ’17-’18 annual dairy imports as a percentage of milk-solids production finished at a four year low value of 3.3%, however ’18-’19 YTD figures have rebounded by 12.4% YOY heading into the final month of the production season.

Aug ’19 U.S. dairy imports as a percentage of milk-solids production declined from the three and a half year high experienced throughout the previous month but remained higher on a YOY basis for the 11th consecutive month, finishing up 9.4%. ’17-’18 annual dairy imports as a percentage of milk-solids production finished at a four year low value of 3.3%, however ’18-’19 YTD figures have rebounded by 12.4% YOY heading into the final month of the production season.

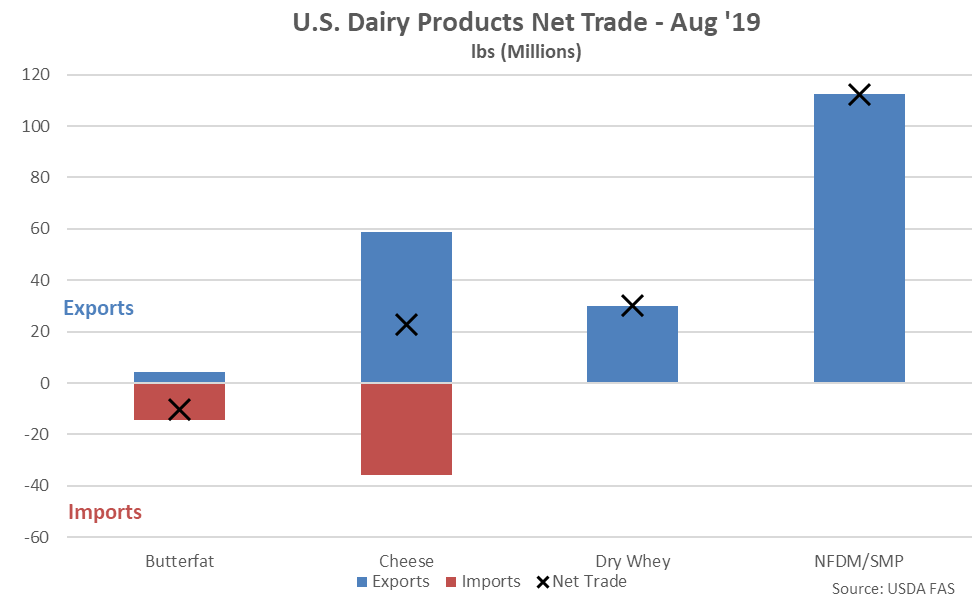

Net trade of U.S. NFDM/SMP continued to outpace that of butter, cheese and dry whey as import volumes remain minimal. Net dry whey trade volumes exceeded net cheese trade volumes for the first time in the past eight months during Aug ’19 while the U.S. finished as a net importer of butter for the 16th consecutive month.

Net trade of U.S. NFDM/SMP continued to outpace that of butter, cheese and dry whey as import volumes remain minimal. Net dry whey trade volumes exceeded net cheese trade volumes for the first time in the past eight months during Aug ’19 while the U.S. finished as a net importer of butter for the 16th consecutive month.

- Aug ’19 U.S. butterfat export volumes declined on a YOY basis for the sixth consecutive month, finishing down 54.6% to a three year seasonal low level while Aug ’19 U.S. cheese export volumes declined 5.9% on a YOY basis throughout the month, also reaching a three year seasonal low.

- Aug ’19 U.S. dry whey and whey protein concentrate export volumes finished lower on a YOY basis on weak Chinese demand, declining by 33.4% and 21.4%, respectively. U.S. whey export volumes destined to China declining by 65.6% on a YOY basis throughout Aug ’19, while whey export volumes destined to all other countries declined by just 5.7%. Aug ’19 U.S. nonfat dry milk/skim milk powder export volumes declined on a YOY basis for the tenth consecutive month, finishing down 18.3%.

- Net dairy trade on a percentage of total U.S. milk-solids production basis declined YOY for the tenth consecutive month during Aug ’19, finishing down 21.5%. Export volumes on a percentage of milk-solids production basis remained lower on a YOY basis for the tenth consecutive month, finishing down 15.5%, while import volumes remained higher on a percentage of milk-solids production basis for the 11th consecutive month, finishing up 9.4%.

Butterfat export volumes destined to Mexico, Canada and the EU-28 declined most significantly on a YOY basis throughout the month, while export volumes destined to South Korea finished most significantly higher.

Canada and Mexico have historically been the largest importers of U.S. cheese, accounting for 55% of total U.S. butterfat export volumes throughout the past five years. U.S. butterfat export volumes destined to Canada and Mexico have declined by 27.0% and 1.6%, respectively, on a YOY basis throughout the past 12 months, compared to a 22.7% YOY decline in U.S. butterfat export volumes destined to all other countries.

Cheese – Export Volumes Decline 5.9% YOY to a Three Year Seasonal Low Level

Aug ’19 U.S. cheese export volumes declined on a YOY basis for the second time in the past three months, finishing down 5.9% to a three year seasonal low level. Cheddar cheese export volumes declined 44.1% YOY throughout the month, more than offsetting a 2.6% YOY increase in other-than-cheddar cheese export volumes experienced throughout the month. ’17-’18 annual cheese export volumes finished up 4.1% YOY to a four year high, despite declining by 4.9% on a YOY basis over the final quarter of the production season. ’18-’19 YTD cheese export volumes remain up an additional 1.6% YOY heading into the final month of the production season, despite the most recent YOY decline.

Aug ’19 YOY declines in cheese export volumes were led by product destined to Australia and Japan, while volumes destined to Indonesia finished most significantly higher on a YOY basis throughout the month.

Mexico and South Korea have historically been the largest importers of U.S. cheese, accounting for 45% of total U.S. cheese export volumes throughout the past five years. Combined U.S. cheese export volumes destined to Mexico and South Korea have increased 0.4% on a YOY basis throughout the past 12 months.

Whey – Total Export Volumes Remain Lower YOY on Weak Chinese Demand

Aug ’19 U.S. dry whey export volumes remained lower on a YOY basis for the 12th consecutive month, declining by 33.4% to a 16 year seasonal low level. ’17-’18 annual dry whey export volumes finished up 12.3% YOY to a four year high, despite declining by 3.0% on a YOY basis over the final quarter of the production season. ’18-’19 YTD dry whey export volumes have declined 30.3% YOY heading into the final month of the production season, however.

Aug ’19 whey protein concentrate (WPC) export volumes finished lower on a YOY basis for the tenth time in the past 11 months, declining by 21.4% to a four year seasonal low level. ’17-’18 annual WPC export volumes finished up 17.4% YOY, reaching a record annual high level for the third consecutive year, despite declining by 4.7% on a YOY basis over the final quarter of the production season. ’18-’19 YTD WPC export volumes have declined 30.6% YOY heading into the final month of the production season, however, and are on pace to reach a four year low level.

U.S. whey export volumes destined to China declined most significantly on a YOY basis throughout the month, finishing down 65.6%. Excluding China, Aug ’19 U.S. whey export volumes declined by just 5.7% on a YOY basis. China applied a 25% retaliatory tariff to a wide variety of U.S. dairy products including whey during early Jul ’18 while Chinese whey demand has also been reduced on weaker feed demand due to African swine fever.

China has historically been the largest importer of U.S. whey products, accounting for nearly 40% of total U.S. whey export volumes throughout the past five years. U.S. whey export volumes destined to China have declined 54.3% YOY throughout the past 12 months, more than offsetting a 0.5% YOY increase in whey export volumes destined to all other countries.

NFDM/SMP – Export Volumes Decline YOY for the Tenth Consecutive Month, Finish Down 18.3%

Aug ’19 U.S. export volumes of nonfat dry milk (NFDM) and skim milk powder (SMP) remained lower on a YOY basis for the tenth consecutive month, finishing down 18.3%. ’17-’18 annual NFDM/SMP exports finished up 16.4% YOY, reaching a record annual high level for the second consecutive year, however ’18-’19 YTD NFDM/SMP export volumes have declined by 12.1% YOY heading into the final month of the production season.

Aug ’19 YOY declines in NFDM/SMP export volumes were led by product destined to Mexico and the Philippines, while export volumes destined to Vietnam and Columbia finished most significantly higher on a YOY basis throughout the month.

Mexico has historically been the largest importer of U.S. NFDM/SMP, accounting for nearly half of all U.S. NFDM/SMP export volumes throughout the past five years. U.S. NFDM/SMP export volumes destined to Mexico have increased 4.5% YOY throughout the past 12 months however export volumes destined to all other countries have declined by 21.3% on a YOY basis over the same period.

Export Volumes Normalized to Production

U.S. butterfat, cheese, dry whey and NFDM/SMP export volumes as a percentage of production all finished below previous year figures during Aug ’19. Dry whey export volumes as a percentage of production finished most significantly lower on a YOY basis throughout the month.

Overall, U.S. dairy export volumes were estimated to be equivalent to approximately 14.2% of total U.S. milk-solids production during Aug ’19 while dairy import volumes were estimated to be equivalent to approximately 3.6% of total U.S. milk-solids production. Aug ’19 net dairy trade finished 21.5% lower YOY, declining for the tenth consecutive month.

Aug ’19 U.S. dairy exports as a percentage of milk-solids production remained lower on a YOY basis for the tenth consecutive month, finishing down 15.5%. ’17-’18 annual dairy exports as a percentage of milk-solids production finished at a record high value of 16.3%, however ’18-’19 YTD figures have declined 13.3% YOY heading into the final month of the production season.

Aug ’19 U.S. dairy imports as a percentage of milk-solids production declined from the three and a half year high experienced throughout the previous month but remained higher on a YOY basis for the 11th consecutive month, finishing up 9.4%. ’17-’18 annual dairy imports as a percentage of milk-solids production finished at a four year low value of 3.3%, however ’18-’19 YTD figures have rebounded by 12.4% YOY heading into the final month of the production season.

Net trade of U.S. NFDM/SMP continued to outpace that of butter, cheese and dry whey as import volumes remain minimal. Net dry whey trade volumes exceeded net cheese trade volumes for the first time in the past eight months during Aug ’19 while the U.S. finished as a net importer of butter for the 16th consecutive month.